Finding winners in this growing megatrend

on Livewire| Original source: https://www.livewiremarkets.com/wires/finding-winners-in-this-growing-megatrend

Note: This interview was taped on Friday 15 November 2024.

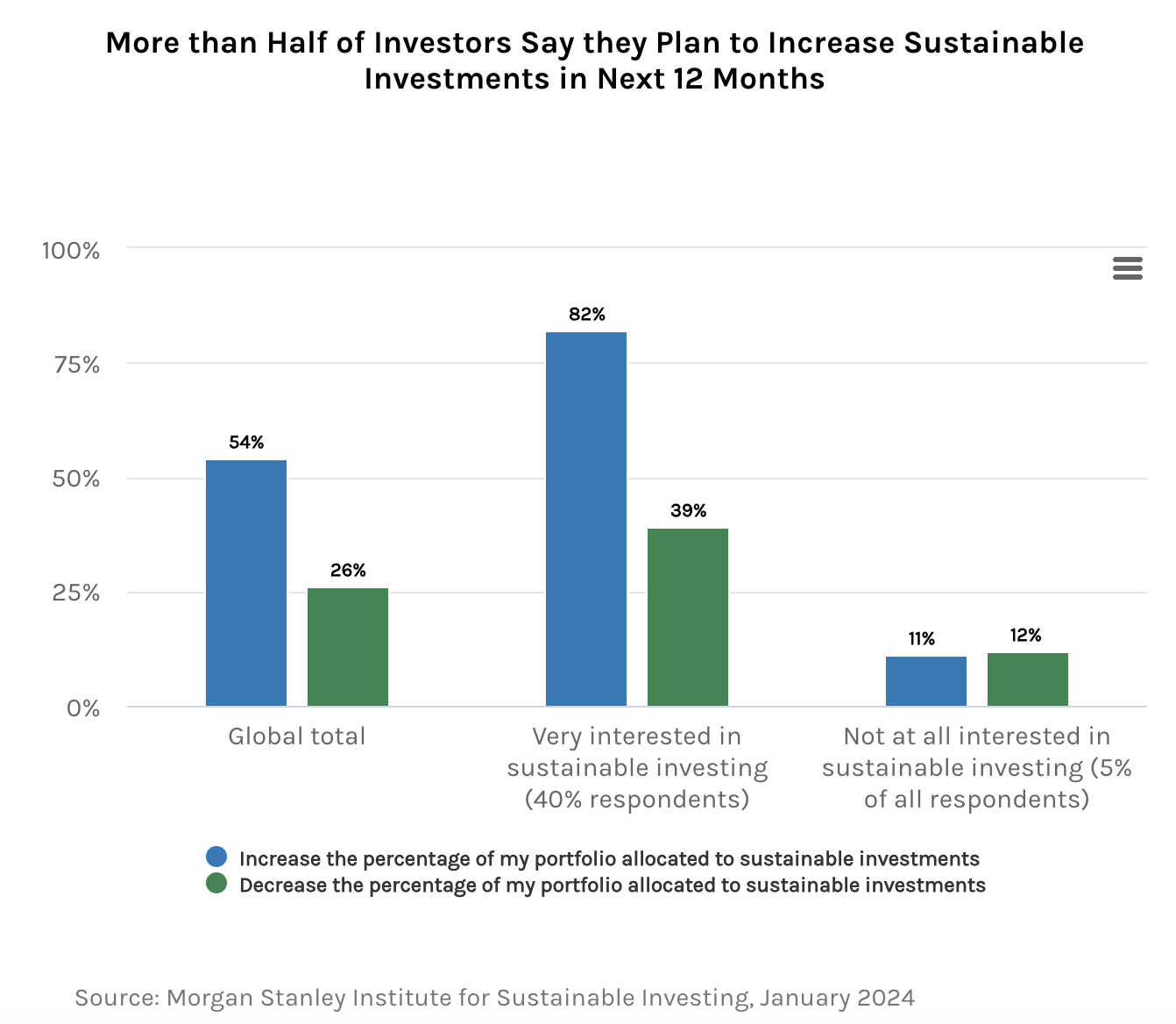

Sustainability - or ESG - investing has seen a massive surge in interest in recent years. Until very recently, that surge was mostly carried by institutional investors like superannuation funds and high-net-worth investors. But, research from Morgan Stanley Wealth Management suggests retail investors are also warming to sustainable investing that reads remarkable even compared to its pre-COVID surge. It found that more than half of individual investors plan to increase their allocations to sustainable investments in the next year.

In addition, for those who are "very" interested in sustainable investing, more than 80% of them are increasing their portfolio allocations to this space.

Source: Morgan Stanley, as of January 2024

Source: Morgan Stanley, as of January 2024

Sustainable investing's themes have also undergone some radical shifts in the last few years. It's no longer the case that sustainable investing is just about investing in companies that are proficient at green-signalling nor is it all about investing in renewables. Sustainable investing is now a truly cross-sector endeavour. Businesses ranging from healthcare companies to education firms and industrial companies are actively seeking more revenues from sources that are linked to the UN's Sustainability Development Goals.

So, to find out how sustainable investing has changed in the last few years (and even longer than that), Livewire's Eddie Orchard sat down recently with Impax Asset Management Senior Portfolio Manager David Winborne.

In this video, Winborne will discuss why he believes this economic transition is worth investing in, where he is finding opportunities in this transition, and will give some examples of the businesses he is backing to make it happen.

David Winborne, Impax Asset Management

David Winborne, Impax Asset Management