The Global Banking Crisis: Is Another Domino Set To Fall?

Chris Watling, Longview Economics

“SVB's failure is a textbook case of mismanagement… The bank waited too long to address its problems… …Our banking system is sound and resilient, with strong capital and liquidity…”

“Absent regulatory action, almost 200 banks were at severe exposure to such runs, as illustrated by the Silicon Valley Bank’ (SVB) failure—the largest bank failure since the Great Recession (Jiang et al. 2023).”

With the failure of both Silicon Valley Bank (SBV) and Signature Bank in March, the US increasingly appears to be at the early stages of a banking crisis.

At the time, the authorities responded with various policy measures* and tried to calm markets with soothing words. In March, for example, Michael Barr blamed ‘one off’ factors for SVB’s failure (see above), while Yellen tried to re-assure markets that the banking system was safe. Policy makers gave similar assurances in the Eurozone crisis and the GFC. This month, though, a third California-based bank has also failed - First Republic - and in recent trading days, there are growing concerns about Western Alliance and PacWest, amongst others as their share prices have fallen sharply.

The key question is, though: Are policy makers right? Are those failures merely a ‘handful of one-offs’, as a result of poor management decisions? Are all the policy tools in place to back-stop stress in the banking system?

Or, as we would argue: Is this banking panic a manifestation of the effects of tight money?

Historically, in that respect, the Fed has tightened until something has ‘broken’. Whilst they continue to tighten and/or keep money tight, it only seems logical that ‘more things will break’ and the banking crisis will deepen and spread.

Arguably, that explains the poor price action amongst the regional banks (whether S&P regional or Nasdaq banks), which have been unable to bounce after their sharp losses in March, and this week have broken down to new multi-year lows.

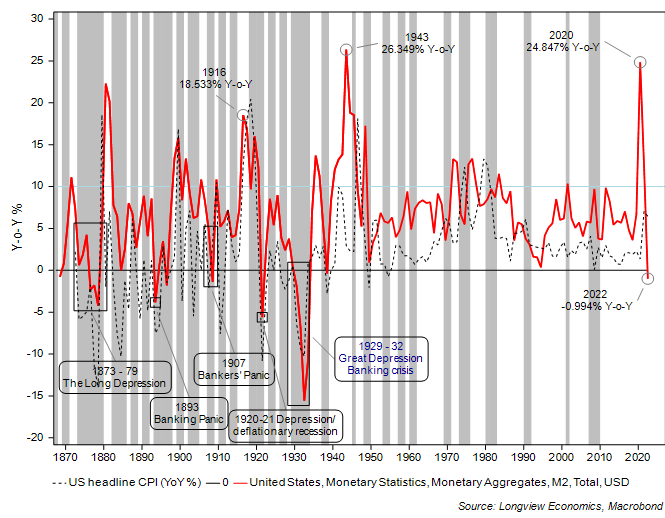

US Money Supply: Shrinking

A deepening of the banking crisis is also consistent with shrinking money supply in the US economy. That is, M2 is contracting on an annual basis for the first time since the Great Depression. In all other examples of shrinking money supply, there’s been a banking crisis, a depression and/or deflation (see FIG 1).

FIG 1: US M2 money supply growth (Y-o-Y %)

Whilst all those prior occurrences happened before WWII, and since then ‘deposit insurance’ has been introduced (1933) and the Fed has become an active ‘lender of last resort’, it’s also the case that M2 money supply hasn’t contracted since the Great Depression. In that sense, the current framework is untested.

Furthermore, the drivers of the money supply contraction are alive and well (as they have been for the past 12 months). Rising interest rates, quantitative tightening and the end of TINA1 (with attractive yielding income products available outside of the banking system), have all contributed to deposits leaving the banking system, see FIG 2 below. That has caused M2 to contract (most of which is bank deposits).

FIG 2: Bank deposits (large vs. small banks) with MMF assets (Y-o-Y change, USD)

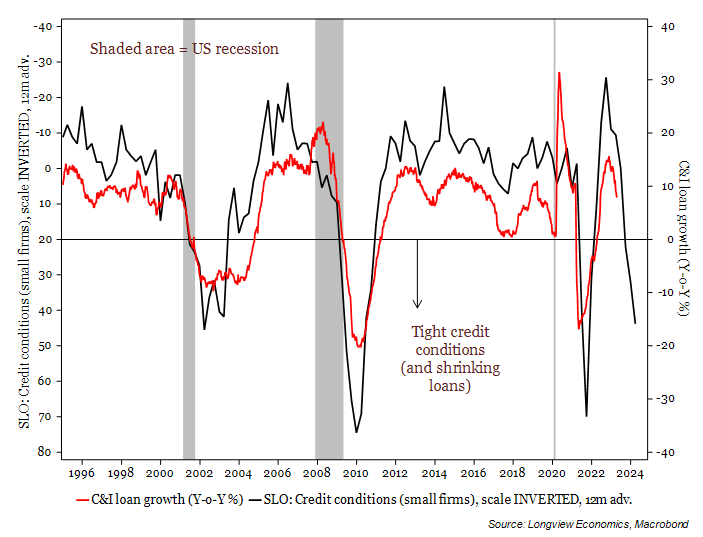

US Credit Conditions: Sharp Tightening Underway!

Unsurprisingly therefore, given that deposit flight (amongst both large and small banks), and despite government measures to provide liquidity, risk appetite in the banking system has deteriorated further in recent weeks. That was well flagged, for example, in April’s Beige Book report, with most Fed districts reporting tighter credit standards and less lending activity.

Coming into this banking panic though, credit conditions were already at multi-year tight levels, consistent with the start of a recession.

The latest senior loan officer reading, for example, (released in February), had already deteriorated to levels which are historically consistent with a contraction in total bank lending (i.e. of about 10% Y-o-Y, see FIG 3 below). When the Q2 data is released on 8th May, which will reflect recent banking system stresses, it will likely point to an (even deeper) contraction in bank lending.

FIG 3: C&I loan growth vs. credit conditions (for small firms, scale INVERTED, 12m adv.)

That contraction, if it happens later this year, should accelerate the cost cutting process in the private sector as companies and households become more cash constrained and are forced to tighten their belts. That retrenching is the heart of the recession dynamic.

The recent tightening of credit conditions, therefore, is one of the main channels by which the banking panic should generate recessionary conditions in the US economy.

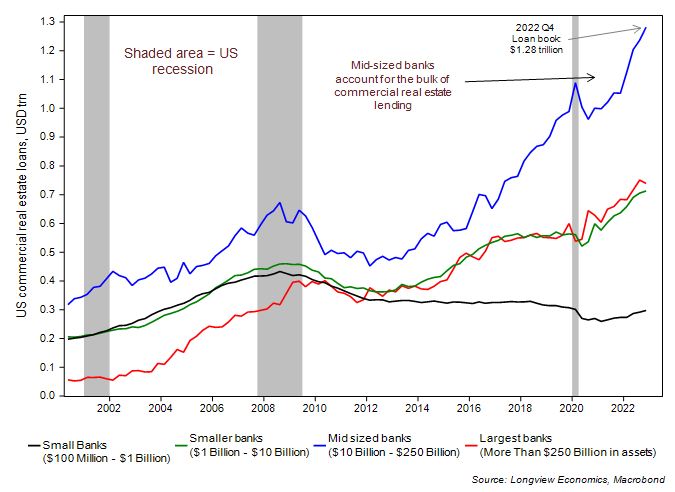

US Commercial Real Estate: The Next Domino?

In that respect, the commercial real estate (CRE) sector is a key area of vulnerability.

In particular, since the GFC**, the mid-sized banks ($10 billion to $250 billion in assets) have doubled their outstanding commercial real estate lending versus that of the large banks (i.e. those banks with assets greater than $250 billion). The latest data shows that the mid-sized banks have a $1.3 trillion commercial real estate loan book, versus $738bn for the largest banks, see FIG 4. With that, their CRE portfolio accounts for 29.2% of total lending.

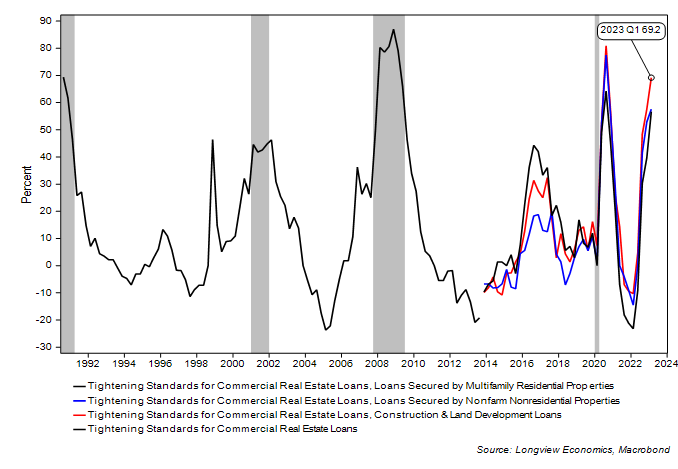

Credit conditions in that part of the banking system (i.e. in CRE) are especially tight (see FIG 6) and, like other types of lending, are probably about to get tighter.

That is happening, though, at a time of record high office vacancy rates. Overall vacancy rates in the top 50 US cities are estimated (by Moody’s) to be 18.8%, just below their record highs in the late 1980s ‘Savings & Loans’ crisis. In New York, property company JLL report the vacancy rate as 15.9%; in Los Angeles it’s 22.5%; in San Francisco it’s 25.1%; while in Chicago it’s 19.5%.

Given those high vacancy rates and low usage of occupied office space reflecting new work from home patterns, the mid-size banks are likely to be hit hard by losses given their high CRE exposure.

FIG 4: Lending to the commercial real estate sector (by key bank size)

This banking crisis is not, therefore, contained, as policy makers and others have been suggesting. A loss of confidence, deposit outflows and losses on securities portfolios are about to be joined by rising delinquency rates in commercial real estate portfolios, especially those of the mid-sized banks. Hits to earnings and further bankruptcies amongst mid-sized banks, therefore, is a sensible central case.

As such, and as per pre-WWII, shrinking money supply growth would then, once again, have led to deflation and a US banking crisis.

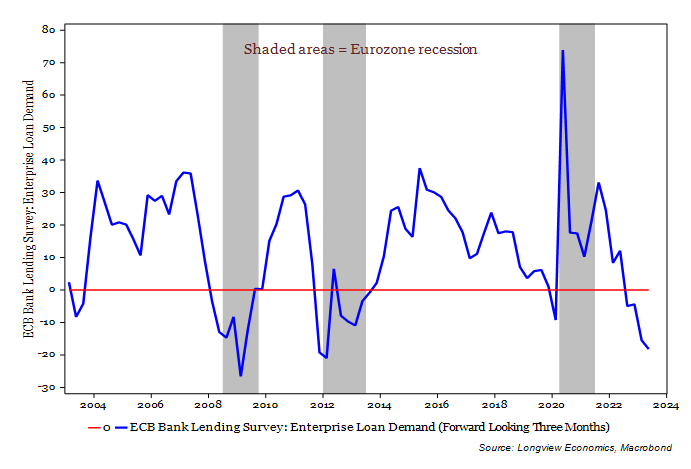

European Banking System: Also Tightening Up…

Whilst the crisis is most obvious in the US, the manifestation of tight money is also emerging in other major economies.

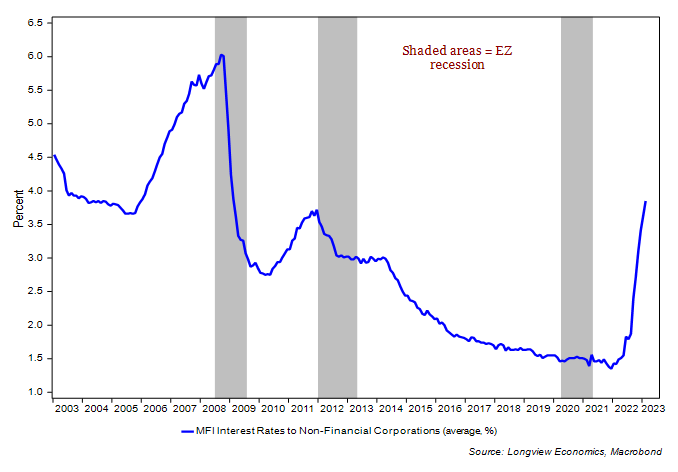

In the Eurozone, for example, the ECB has raised rates by 350bps in just the past 10 months, with another 25bps hike expected this week (and another 25bps next month). This tightening phase is therefore the largest and fastest in ECB history.

Illustrating the speed of tightening, lending rates to non-financial corporates are now at 3.85%, up from 1.35% as recently as December 2021, and up 250bps in just 14 months (FIG 7). Elsewhere mortgage rates have risen significantly (depending on the country). Unsurprisingly, therefore, high rates have markedly weakened demand for credit, with surveys showing that business and household loan demand is at multi year lows, and at levels consistent with a turn in the credit cycle and a recession (e.g. see FIG 5).

FIG 5: Bank Lending Survey: Enterprise Loan Demand (three months ahead)

FIG 6: US SLO survey lending standards for commercial real estate loans

FIG 7: Average MFI interest rate to nonfinancial corporations (%)

1 There is no alternative.