Lessons from 2020 for yield hungry investors

Sinead Rafferty CFA, Investment Specialist, Fidante Partners

After a tough 2020 for income focused investors, the outlook looks brighter as a new year dawns. Of late, dividend income has been subdued at best as the impact of the pandemic led many companies to slash or abandon dividends altogether. While the share prices of companies listed on global equity markets have rebounded from the early 2020 losses, dividends have been slower to recover. In the Australian share market, the dividend cuts have been stark, with 62 companies in the ASX 200 cutting their dividend and 40 suspending it altogether1. As the global economy and company earnings recover, the ability of corporates to increase dividends is expected to improve. Using the bank sector as a case study, we reflect on the outlook for dividends as part of the total potential return as well as the prospects for future dividend growth.

There are several considerations when assessing the attractiveness of the income stream associated with an equity investment.

- In a low interest rate environment, there is a scarcity of income sources and on a relative basis, returns on Australian shares are considerably higher than those available on cash and most other defensive assets.

- Investors need to be mindful not to have a myopic focus on income. It is understandable to prefer spending dividend income rather than capital gains, however depending on the tax rate of the investing entity, either may provide the same net return.

- Investors who look more broadly across sectors for income and choose dividend growth rather than historical yield are more likely to outperform over the long run.

- Higher yielding stocks can offer an attractive risk-return trade-off when valuations are considered. Many of these stocks have underperformed in recent years and will benefit if the much-hyped rotation into value stocks that we saw in the last quarter of 2020 continues.

Relative returns

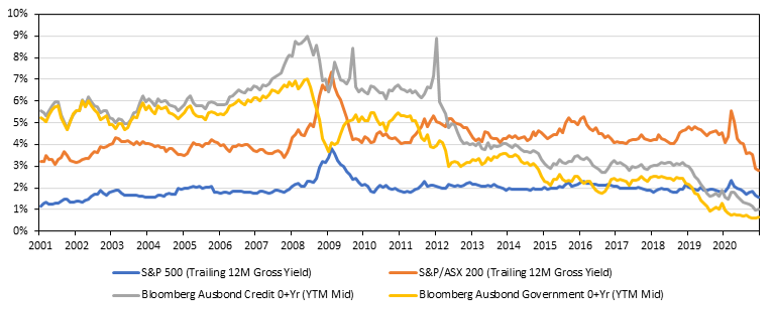

Australian shares have historically paid a higher yield than global peers. Australia’s dividend imputation system incentivises corporates to maximise the franking credits available to their shareholders. Franking credits provide an offset for investors of the corporate tax paid by the company so that tax is not paid on company earnings twice. This skews the return investors receive on Australian shares to be more focused on income than capital gains. Over the past 30 years, the long-term average yield on the ASX 200 was 4.1%, as shown in Chart 1. Although this is projected to be lower in the coming months as the secondary impacts of the pandemic are felt, it is still attractive when compared to the US share market for example, with a historical dividend yield of 1.9%, and other asset classes such as bonds and cash.

Chart 1: Equity vs. Bond Yields

With the cash rate at 0.10%, and interest rates set to stay low for several years, many investors are moving up the yield curve in search of returns. As Chart 1 shows, the income return from Australian shares is increasingly more attractive on a relative basis than other defensive options such as government bonds and credit.

Focus on Total return, not the current yield

In Australia, many self-funded retirees have been attracted to the banking sector which has paid out up to 90% of their earnings as dividends historically. Combined with franking credits, the income generated from dividends has contributed to meeting their income needs. However, the capital return for the sector has been poor for the last 5 years, with the banking sector providing little or no price growth. The ASX bank sector 5-year total return was 3.42% compared to 10.03% for the ASX 200 overall2. Despite the attractive relative yield, the total return has underperformed the broader market.

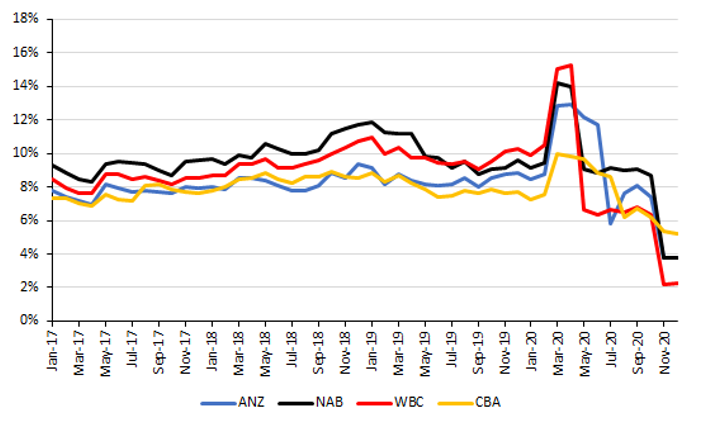

A weakening economic environment brought on by the COVID-related restrictions meant APRA encouraged the banks to reduce their payouts and shore up their capital. At the time, forecasts were for a dramatic increase in unemployment and large-scale defaults by both mortgage holders and small business owners. Chart 2 shows the impact of both the fall in share prices in March 2020, which boosted the reported dividend yield, and then the subsequent fall in yields as dividend cuts were implemented. Investors were impacted by both the fall in income as well as the fall in share prices.

Chart 2: Big 4 Banks - Trailing 12M Gross Dividend Yields

While some sectors of the economy have been profoundly impacted, the Australian economy as a whole has held up better than expected. The RBA now expect unemployment to peak at a little below 8% compared to their forecast of 10% in March3. As such, it could prove that banks have over-provisioned for bad debts. If the economy continues to improve, we could see much of this wound back over time, increasing earnings and the ability to pay more to shareholders through dividends and share buybacks. APRA recently revised their guidance to banks regarding their payouts, lifting the restriction for banks to cap dividends at 50% of profits.

While we are not out of the woods yet and low interest rates are likely to keep net interest margins compressed, the outlook for dividends is healthier than it was six months ago. The combination of a cyclical recovery of the Australian economy, which is likely to increase the demand for credit, potentially boosting share prices as well as the unwinding of restrictions on payout ratios improves the outlook for the sector on a total return perspective.

The need for growth

As investors consider what a post-COVID world will look like and the long-term impact on various sectors, those looking for income should consider which stocks are growing their yield and not merely their historical yield. Will the leaders of the future look different from the past and how much diversification is appropriate?

While some stocks that were previously overvalued may now be attractive to income seeking investors at their new lower entry levels, new industries are emerging that may alter perceptions of what constitutes a blue-chip stock. Maturing companies that were previously focused on growth, often increase their payout ratios over time. Some mining companies who have benefitted from higher commodity prices have maintained or increased their dividends. For example, Fortescue Metals announced a bumper dividend in 2020 on the back of higher iron ore prices. Parts of the recovering retail sector also offer attractive yields due to higher earnings as households are spending more of their discretionary income on their home with travel and dining limited. While dividends may be lower in the short-term, looking more broadly across sectors of the market can provide a steady income stream for investors.

A risk that investors need to consider when investing in income-producing shares is the sustainability of the yield. Is the dividend yield rising because the business is growing and increasing dividends over time or does the rising yield merely reflect the flip side of the equation – a falling share price? The varying fortunes of the underlying businesses is a key consideration especially as many yield hungry investors think ‘there is no alternative’ to investing in shares. An assessment of dividend and earnings sustainability is fundamental to the successful management of a share portfolio. These considerations are a core tenet of professional investing and part of an active manager’s investment process.

Summary

- Income from Australian shares remains attractive relative to many other asset classes.

- Investors need to be mindful of biases leading them to prefer income over capital returns – consider total return.

- A share portfolio that includes companies delivering dividend growth from sustainable cash flows is likely to offer better long-term returns.

2. Source: S&P Dow Jones Indices as at 29 January 2021

3. https://www.rba.gov.au/publications/smp/2020/nov/economic-outlook.html

This material has been prepared by Fidante Partners Limited ABN 94 002 835 592 AFSL 234668 (Fidante) for wholesale investors only. It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information.

Any projections are based on assumptions which we believe are reasonable, but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed.