Market Musings: The Tipping Point?

Ardea Investment Management

This article was first published on Ardea Investment Management.

- March bank stress is not a repeat of 2008, but downside risks remain.

- We discuss the underlying drivers of historically high volatility in interest rate markets.

- The potential path ahead for rates is wide, underscoring the value of defensive, macro neutral strategies.

Bank stress is not GFC 2.0, but downside risks remain

March was eventful in markets. The collapse of SVB, forced merger between Credit Suisse and UBS and pressure on other banks was a major shock for investors. Volatility surged – most notably in interest rate markets and US regional and some European bank assets. Bank failures, forced mergers and emergency liquidity provisions has a 2008 feel about it.

Since the initial shock, investor sentiment has moved towards a “this time is different” view. And with some good reasons, notably:

- Idiosyncratic risks with the business model and capital structure of SVB and other US regional banks.

- The substantial improvement in capital and liquidity positions of large, systemically important banks since 2008.

- The rapid response of policymakers to shoreup confidence – through heavy liquidity provision and assurances to deposit-holders.

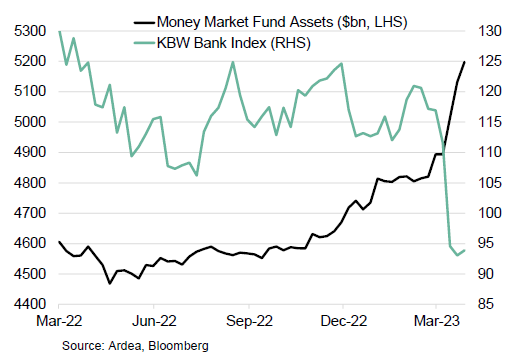

Market panic has eased significantly over the last week, but it’s still early days. Markets will remain wary about liquidity and profitability of banks at a time of high short-term rates. Smaller US bank stock prices have taken larger hits in March and there have been large deposit flows from smaller to larger banks and to money market funds where pricing is attractive (Chart 1). Technology has facilitated faster deposit flows than in 2008, as the speed of collapse in SVB shows. Broader funding market stress has been well contained, supported by ample central bank liquidity.

Chart 1: Regional US bank stock index and money market fund assets

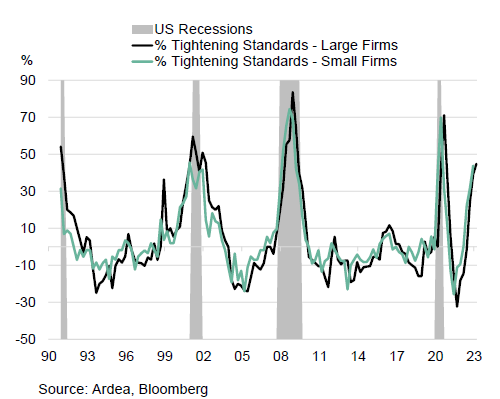

Assuming markets continue to move past the panic of March, downside risks for the economy could linger in the form of tighter credit conditions. That pressure could add to the material tightening of lending standards already evident ahead of the SVB collapse (Chart 2). There have also been underlying concerns about particular sectors of the economy, such as commercial real estate. Some analysts suggest further credit tightening could be worth up to a 0.5ppt hit to US GDP growth.

Chart 2: Fed Senior Loan Officer Survey - % of US banks tightening credit standards

A massive shift in rates markets

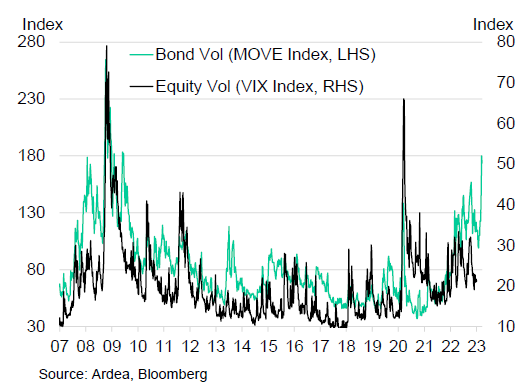

Interest rates have been one of the biggest movers over the last month. Broad measures of bond volatility returned to 2008/09 levels, while in equities, volatility remains below most prior periods of market stress.

Chart 3: VIX vs MOVE index

The moves in rates markets have been especially violent at the front end of the curve and more in the US than other markets. Of note:

- Implied swaption volatility on USD 1y swap rates with 1y expiry eclipsed 2008 highs.

- The US Treasury 2y yield tracked a 160bp range – falling from over 5% to sub-4% midmonth and registered one of the biggest ever 3 day moves.

- The UST 2s10s curve steepened the most in a single day since the early 1980s.

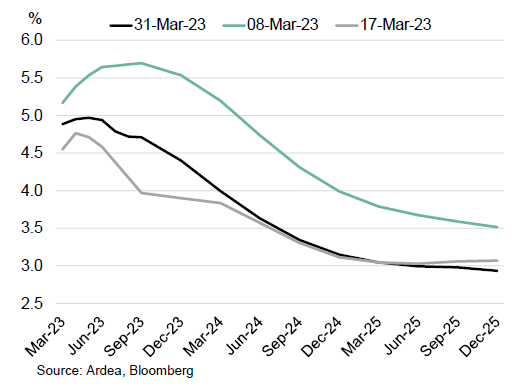

- For the end of 2023, the market moved from pricing nearly 100bp of Fed rate hikes to as much as 80bp of rate cuts (Chart 4).

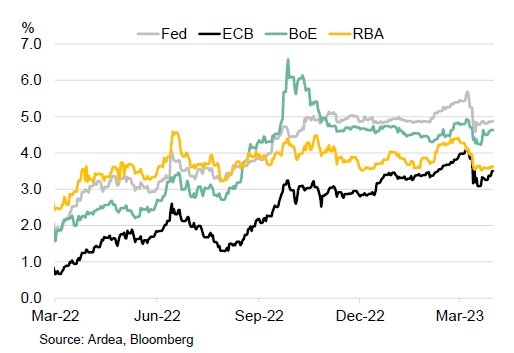

- Other markets moved by less than the US, but the repricing of terminal cycle rates was still significant for the ECB, BoE and RBA (Chart 5).

Chart 4: US 3m forward rate curve (SOFR)

Chart 5: Central bank terminal rate pricing

Why is relative volatility so high in rates markets?

There are four main reasons relative volatility has been so high in rates markets:

- The higher for longer rates starting point. Heading into March, markets had priced more aggressive tightening as inflation and activity data exceeded forecasts. That left the rates market with further room to rally. The starting point had also pushed duration positioning short, particularly among hedge funds, adding to the bond rally.

- The perceived narrow nature of the crisis. As outlined, markets see a lower risk of spillover into larger systemically important banks that have a bigger weight in broader equity and credit indices.

- Credit vs monetary tightening. The prospect of further tightening in credit conditions is seen as a substitute for rate hikes.

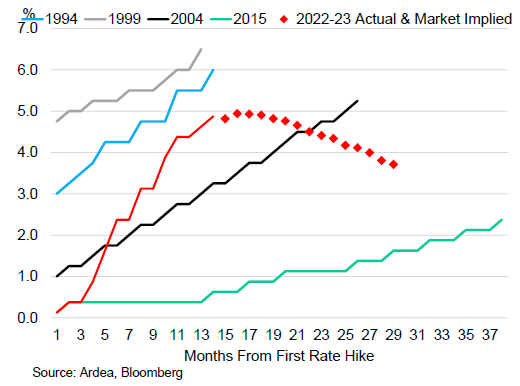

- Historical precedent. Nearly all prior Fed hiking cycles have led to some form of broader financial market correction or crisis and not always centered in the US. Simply, the Fed tends to break something and as Chart 6 shows, this cycle has been more aggressive than previous cycles (for example, the 2018 risk-asset correction, 2007-08 housing collapse and GFC, in the 90s the dot com bubble and Asian financial crisis).

Chart 6: Fed cycles compared

A wider path ahead for rates

Over the last month, the Fed, ECB, BoE and other central banks continued to hike rates and reduce bond holdings in the face of high market volatility, for two main reasons:

- Meeting the inflation objective and emphasizing the use of separate tools to deal with financial instability (such as liquidity facilities, which in some cases offset some of the reduction in balance sheets coming from quantitative tightening).

- Supporting sentiment – a pause in rate hike plans could detract from confidence.

The outlooks from most central bankers, including actual rate projections from the Fed, are well above the market. For example, the median FOMC member rate projection is 1- 1.25% above market pricing for 2023 and 2024 (Chart 7). Many market economists are similarly unconvinced of lower market pricing.

Chart 7: Market pricing for rates vs FOMC projections

It’s worth noting a key difference between how economist (Fed or private sector) and market rates expectations are formed. Economists typically make calls for rates based on the path for the economy they see as the most likely. In the current context, most think a serious contagion or imminent deep recession will be averted. By contrast, market pricing is better thought of as a probability weighted average of a distribution of possible outcomes. There is now more weight in the left tail for rates outcomes, accounting for the risk of further banking sector stress, how tighter credit conditions flow through economies and the possibility of some other sector coming under pressure.

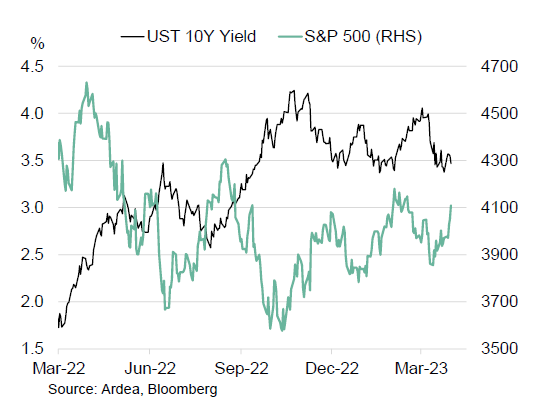

This larger left tail means bonds may continue to look expensive vs many base case rates views in the near term. The recent divergent paths between equities and bond yields (Chart 8) suggests equities are either less worried about recession risks or are putting more weight into the probability of lower rates (although there is significant sector dispersion within indices).

Chart 8: Equities vs bond yields

It’s worth remembering just a few weeks ago the other side of the distribution – higher for longer rates – was the dominant market narrative. Core inflation is running around 5.5%pa across major economies and is yet to moderate enough to give central banks confidence in a policy pivot. Against this backdrop, it’s possible for any easing of growth concerns to quickly bring inflation back into focus.

As outlined in our 2023 themes note, the scale of macro uncertainty in both directions on rates is substantial and can keep rates volatility well above normal levels this year. In an environment where bonds are now delivering yield again, investors need to remain wary about volatility assumptions, even for short duration fixed income.

The current market environment underscores the value of strategies independent of subjective macro rates views (we noted here how macro uncertainty tends to increase interest rate RV mispricing). And the use of interest rate option strategies can help navigate stressed markets (see here for more detail).