The next three years of the AI rally will come from these stocks

on Livewire

Note: This interview was taped on Friday 15 November 2024.

There is no doubt that artificial intelligence, the story of 2023, has also been a leading narrative in 2024. But despite Nvidia trading on a trailing P/E ratio of 66 and main rival AMD having a trailing P/E ratio of 119 (!), it's clear the demand for these game-changing stocks is still alive and well.

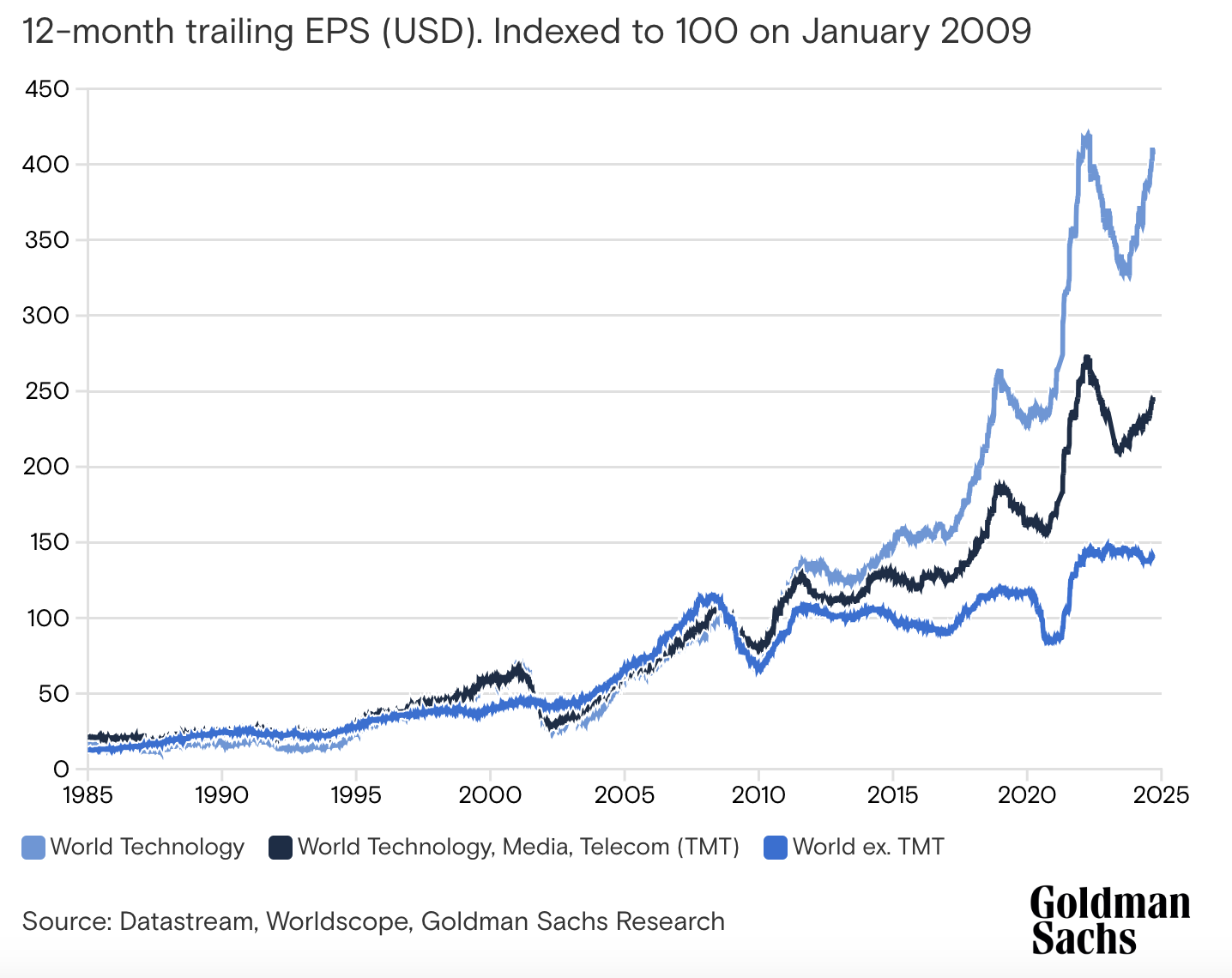

One such firm that believes the AI rally has even more legs to run is Goldman Sachs. In a note entitled "AI stocks aren't in a bubble" from September 2024, Goldman's Peter Oppenheimer noted that tech earnings have far outpaced the rest of the market and so have earned their right to be this valuable.

Source: Goldman Sachs

Source: Goldman Sachs

But, Oppenheimer also pointed out that it is also an opportune time to look away from the Magnificent Seven.

“Investors should look to diversify exposure to improve risk-adjusted returns while also gaining access to potential winners in smaller technology companies and other parts of the market, including in the old economy, which will enjoy the growth of more infrastructure spend,” Oppenheimer said.

“Eventually the market for the original technology tends to consolidate into a few large winners, and the growth opportunity shifts to secondary innovations or products and services that follow the original technology,” he adds.

Those secondary innovations or products can be referred to as the infrastructure providers in the AI megatrend. After all, the data has to be crunched somewhere! And in this case, it has to be crunched in a factory that is often very hot, requires a lot of power, and needs a ton of equipment. These are the AI "enablers".

But now the "enablers" have seen such a big run, the next leg of this story, according to David Winborne of Impax Asset Management, will be told in the AI "implementers" category. These are the companies that are racking up huge CAPEX now but will see their application bear fruit in the years to come.

To find out more about Winborne's thesis and one stock he is backing with this theme in mind, watch this episode of The Pitch, presented by Livewire's Eddie Orchard.

David Winborne, Impax Asset Management

David Winborne, Impax Asset Management