When the rising tide that lifts all boats subsides

Kapstream Capital

This year has been a sea of red for many traditional asset classes. In the equities space, the S&P 500 has fallen as much as 20% from the highs seen around the turn of the year. Government bonds have also sold off, with yields rising by more than 200bps in some cases since the 2020 lows, with most of that occurring since the start of 2022. Investment grade corporate bonds have additionally suffered as credit spreads have drifted around 50bps wider from their late 2021 lows. Property prices are starting to record falls in some areas. Even less traditional asset classes such as cryptocurrencies have not been immune, with Bitcoin down more than 50% from its November peak. Only commodities seem to have weathered these tidal currents, rising under a perfect storm of pandemic-related supply side constraints and geopolitical events such as the invasion of Ukraine.

Usually when tides shift, water flows from areas of low tide to areas of high tide. This raises the water level in one region at the same time it recedes from somewhere else. Financial markets typically display a similar phenomenon. At times of heightened fear, investors shift toward defensive asset classes such as bonds and shy away from riskier assets such as equities. The converse tends to happen when times are good. Higher earnings expectations boost the demand for equities, while bonds sell off as rate cuts are unwound. This tends to see the price of risky and defensive assets move in opposite directions.

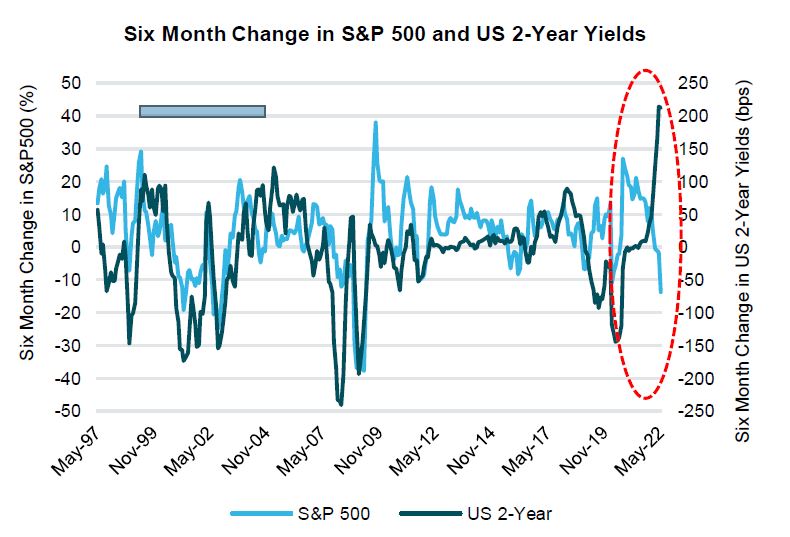

One way to show the usual historical correlation between bonds and equities is to look at the six month change in both the S&P 500 and US two year Treasury bond yields. The chart below shows the two normally move together. That said, periods where yields and equities don’t move in lockstep are not uncommon. For example, leading into early 2008 and the global financial crisis, US yields fell significantly as the Fed started cutting rates but equities continued to rise. However, these periods don’t tend to last for too long before the more usual correlation re-asserts itself.

What is so unusual about the experience so far in 2022 is that returns on risky and defensive asset classes have moved significantly down together. Short-term rates in the US have risen by more than 200bps in the past six months – a pace unparalleled in the past 25 years. The fall in equities has been significant but not quite as extreme. The up to 20% fall from the peak in the S&P 500 puts it in the second tier of risk-off episodes, but still some distance from the 35-60% size sell offs seen during the GFC or at the start of the pandemic. Nonetheless, it is that these occurred at the same time that is relatively unique. For example, April represented only the 4th month in almost 50 years that equities and bonds both fell substantially1.

So what caused the ‘tide that lifts all boats’ to so suddenly subside? We see it as largely due to the unwinding of the emergency stimulus that was introduced at the start of the pandemic in early 2020. The cuts in official interest rates and bond purchase programs have not just stopped but are now being unwound. The significant boost from fiscal policy is also fading. Both of these processes have been hastened as labour markets have recovered much more quickly than seen in previous recessions. This has resulted in the higher and non-transitory inflation becoming the dominant concern. The significant expansion of the amount of money in the system, due to cheap borrowing costs and central bank bond purchases (which had boosted asset prices) is now starting to flow out of the system. The tide is drifting out, and just as it did on the way in, it’s impacting the price of many asset classes simultaneously.

Implications for investors

Asset allocation based on the usual historical negative correlations between risky and defensive assets have unsurprisingly performed poorly. Risk parity style approaches to portfolio construction, such as the 60/40 split between equities and bonds, have seen marked declines into the double digits in many cases. It’s perhaps not surprising that when an unusual and temporary positive correlation between risky and defensive asset returns resulted in both sleeves of ‘balanced’ portfolios going up in value, investors did not pay the same attention as today, where positive correlation has driven both sides of the portfolio down.

The fixed income space is no exception, with traditional benchmark-aware funds not faring well. The Bloomberg AusBond Composite Index lost a further -1.49% in April and is now down more than 7% calendar-year-to-date. These are enormous declines that are normally seen in the equity sleeve of portfolios, again, at a time when equities themselves have been falling.

Such large declines are a result of these fixed income portfolios being based on a benchmark that is dictated merely by the amount of bonds on issue. There is no efficiency or capital preservation underpinnings in the construction of these benchmarks. For example, as the Australian Government has issued more debt and extended maturity dates out to around 30 years, the duration of the benchmark has increased from around 3.5 years in 2011 to be around 6 years late in 2021. This significantly increased the sensitivity of such portfolios to the inevitable interest rate tightening cycle that is now underway. It is effectively impossible for active decision-making within these funds to offset the large declines in the benchmark when bond yields rise as quickly as they have recently.

Absolute return fixed income portfolios tend to have a larger exposure to corporate bonds rather than government bonds, largely on efficiency grounds. Such funds can also have a modest exposure to interest rates as a hedge. However, even here some common combinations would not have fared well so far in 2022. For example, a portfolio with an exposure to shorter-dated investment grade corporate bonds of around three years spread duration, when combined with one year of interest rate duration, still would have lost close to 200bps so far this year. Any product design based on a philosophy of simply picking up the higher returns from lower quality or longer duration corporate bonds than used in this example would have fared much worse.

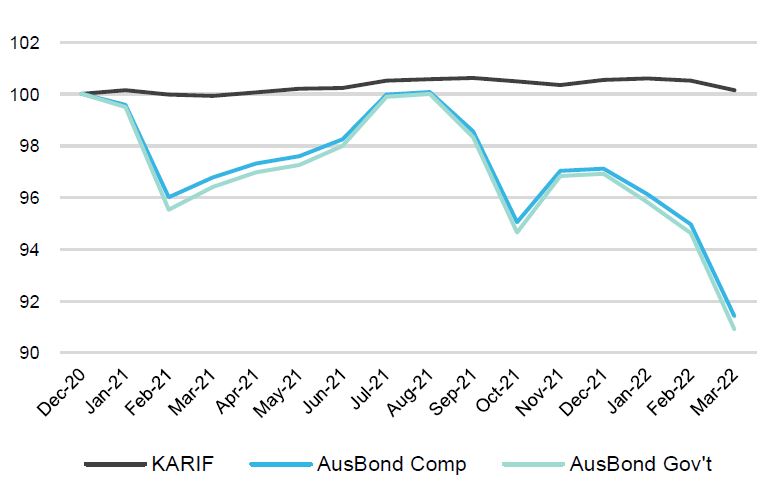

In this context, a period such as that we have been through highlights just how important the benefits of an all-weather product design focused on absolute not relative return and active management can be. Whilst we acknowledge that any negative returns are never good for investors and look to avoid these whenever possible, we believe that the return enhancement and capital preservation components of our approach has limited the extent of losses during this highly unusual period. The chart below shows how this has played out for investors in an approach like Kapstream’s relative to more benchmark aware products.

Concluding thoughts

Warren Buffet’s famous quote that “only when the tide goes out do you discover who’s been swimming naked” has never been more apt. The experience of many portfolios in the calendar-year-to-date period has seen which investment philosophies have unduly relied on typical historical correlations and others that are merely based on inefficient or overly risky elements.

What has also been highlighted is the need to find a manager that not only understands the products they manage and the market environment in play, but one that is able to take advantage of this over the cycle in order to meet investor’s objectives. While we do not enjoy periods where our Fund is likely amongst the best performing funds an investor can select, it has demonstrated a suitably defensive design in preventing the significant declines that have befallen other funds.

To finish on a positive note, the challenges faced this year also present an opportunity looking forward. Rising rates are not necessarily a bad development. For over a decade, we’ve all moaned about astonishingly low bond yields. Important at this juncture is the pace of yield rises which will dictate the trajectory of bond returns. Without short term surprise (please central bank Chairs and Governors, take note) investors have the opportunity to reinvest maturing securities at yields higher than what had been available only weeks or months prior. This strategy is all the more relevant for approaches (such as ours) biased to shorter-dated assets that can exit highly liquid positions and reallocate towards longer-dated, higher-yielding securities of similar quality. If inflation proves more persistent than expected but policy rates remain on hold, shorter-dated strategies and/or those with active mitigation of duration sensitivity are also less impacted by rising rates than those that have extended duration profiles.

The higher yields that fixed income portfolios now exhibit also provide more coupon income to act as a buffer than that which existed in the zero interest rate world. The return of the usual negative correlation between rates and credit should therefore make fixed income funds more relevant than they have been in the recent past, if risk markets were to deteriorate further. We expect that this negative correlation will return once peak inflation and peak hawkishness from the central banks subsides. It’s arguable that we are already at that point, raising the usefulness of a stable defensive component to an investor’s overall asset allocation. Regardless, it will remain vital for investors to learn how to survive in shallower water, and more importantly to be prepared for unexpected changes in tide!